What's 🔥 in Enterprise IT/VC #253

What's 🔥 in Enterprise IT/VC #253

📈 The future of enterprise software is ☀️ - MongoDB, Asana, Okta - 🦄 or 🐲

Given that it is Q2 earnings season for some of the bellwether tech companies in infrastructure, developer, and SaaS markets, I wanted to continue my thread from last week. Yes, valuations are at all time highs, there is so much pent up demand in the private markets to fund 🦄 in search of the next 🐲 (see below) and growth is what matters. While I’ve been working with enterprise founders from Day One for over 25 years and feel valuations are high, what gives me comfort is IT Spending. With that, I like to read between the lines, not just looking at earnings but also what the CEOs are telling Wall Street about what’s ahead - are choppy waters ahead for those companies or are they more optimistic, especially given the Delta variant? I’ve extracted a few notes from MongoDB, Asana, and Okta to start.

Here’s the short optimistic version for the road ahead:

MongoDB - We believe our strong second-quarter results are a clear indication that customers view MongoDB as a critical platform to accelerate their digital innovation agenda.

Asana - We are currently experiencing one of the biggest workplace transformations in history

Okta - These factors, combined with the ever-evolving security threats, landscape, meaning that the demand for Okta's modern identity solutions has never been greater.

Conclusion - 2021 is looking darn good and lots of IT 💰 up for grabs in developer infra and productivity, SaaS, and cybersecurity!!!

Longer versions below along with links to transcripts.

MongoDB - win the ❤️ and 🧠 of developers and win the enterprise

Looking quickly at our second-quarter financial results, we generated revenue of $199 million, a 44% year-over-year increase and above the high-end of our guidance. We grew subscription revenue 44% year over year. Atlas revenue grew 83% year over year and now represents 56% of our revenue, and we had another strong quarter of customer growth, ending the quarter with over 29,000 customers. Businesses across nearly every industry have realized that in today's highly dynamic global markets, speed of development is a meaningful competitive advantage.

Businesses that can develop software faster are able to improve their products faster and ultimately, grow more quickly than their competition. We believe our strong second-quarter results are a clear indication that customers view MongoDB as a critical platform to accelerate their digital innovation agenda. Customers of all types are choosing MongoDB because they can develop so much faster using our platform to build new applications and replatform legacy applications across a broad range of use cases to drive their business forward. Fundamentally, MongoDB's application data platform offers three intrinsic advantages.

First, MongoDB's document model is designed around developers think and code unlike legacy data technologies.

Asana - collaboration software and workplace productivity

We had another great quarter in Q2. We accelerated revenues, accelerated enterprise customer growth and increased dollar-based net retention rates across the board. Revenues of $89.5 million grew 72% year-over-year, accelerating 11 percentage points versus Q1. This is a very significant acceleration and the third quarter in a row of acceleration. We are now at a $358 million GAAP revenue run-rate.

As everyone is probably well aware, we are currently experiencing one of the biggest workplace transformations in history. Even after a year of surprising changes, the situation remains fluid. It can be difficult to achieve organizational wide clarity under normal circumstances. And for the past 18 months, this challenge has hit an entirely new level. The reality of the moment is that increased workloads and too many emails, messages, meetings and video calls are barriers to productivity. According to our annual survey called the Anatomy of Work, limited employee bandwidth has meant that over one-fourth of deadlines are missed. A key driver is the lack of clarity caused by unclear processes. Large enterprises, in particular, delays in the inability to successfully pivot as needed can add up to a significant drain on resources, revenue and profitability. While the symptoms around these types of pains have evolved, their root causes have been with us for a long time. Through it all, Asana’s mission to help humanity thrive by enabling the world’s teams to work together effortlessly has remained constant.

Okta - the identity and access management company for secure access

Regardless of the timeline, it's clear that most organizations are adopting plans that include more remote access. Organizations also realized that their interactions with customers will continue to shift more online and need to accelerate their digital transformation business plans.

These factors, combined with the ever-evolving security threats, landscape, meaning that the demand for Okta's modern identity solutions has never been greater. I'll start with a quick recap of our Q2 financial results and then get into some of the other notable highlights from the quarter.

To highlight just a few of our second-quarter financial metrics, revenue growth for both standalone Okta and Auth0 were strong, which produced combined Company revenue growth of 57% and subscription revenue growth of 59%.

RPO surpassed the $2 billion milestones. For reference, it took Okta 10 years to reach the $1 billion RPO milestone and less than 2 years to hit the $2 billion milestones. That's tremendous progress. The current RPO also reached a milestone by surpassing the $1 billion mark. Our total base of customers now stands at over 13,000.

Okta Standalone added 750 customers, which is a record for any quarter. Also, included in the base is the addition of 1,650 off zero customers net of common customers. Our total base of $100,000 plus average contract value customers or ACV, now stands at over 2600. Okta's standalone added 160 new $100,000 customers, and once again, half of the brand-new customers.

And off to 0 brings 375 $100,000 customers to the base.

As always, 🙏🏼 for reading and please share with your friends and colleagues.

Scaling Startups

Founders, raising more money right after you raised weeks or months prior is great, right? Well, frankly one issue that is not talked about enough is below 👇🏼

It’s easier to raise money than get a story in TechCrunch - prep accordingly

No conflict, no interest? An important read for founders as VCs raise even more capital and expand their strategies - what does it mean to invest in a competitor?

Secrets of the best performing teams 🧵

YC Summer 21 - 377 companies

🐲 or 🦄

@danprimack Let’s go 🐲. Some of us in VC industry though think of 🐲 as companies that return the whole fund. Depending on size of fund and ownership a 🐲 does not have to be a 🦄. Regardless the point for a 🐲 regardless of private co > $12B or fund returner, they are rare

@danprimack Let’s go 🐲. Some of us in VC industry though think of 🐲 as companies that return the whole fund. Depending on size of fund and ownership a 🐲 does not have to be a 🦄. Regardless the point for a 🐲 regardless of private co > $12B or fund returner, they are rareAnd even better - a 3x fund maker!

Here’s the complete list of 🦄 from CBINSIGHTS.

Enterprise Tech

I do agree that founders in their first sales often are just happy to have a paying customer and don’t ask for enough to start - from Mitchell at Hashicorp 🧵

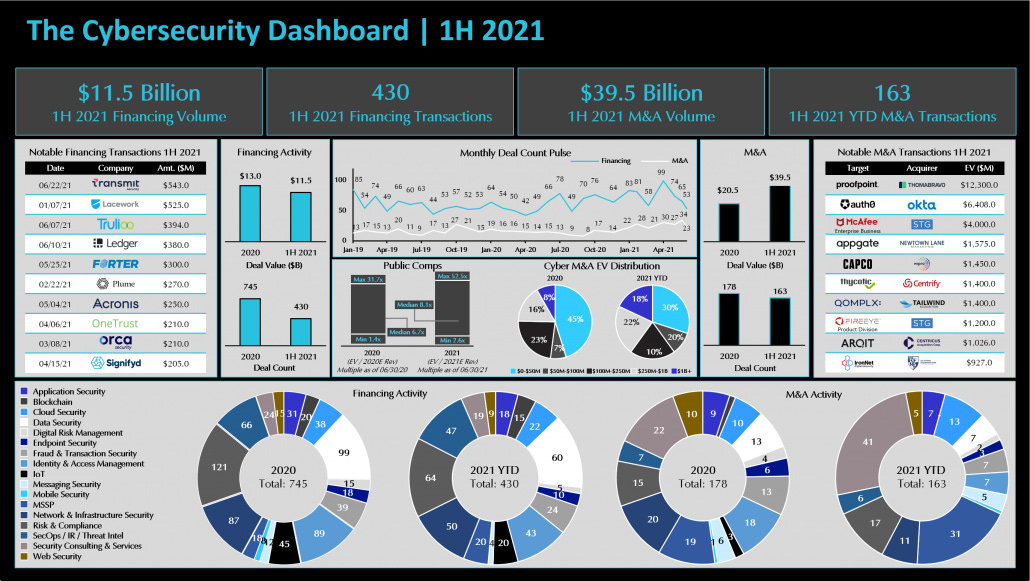

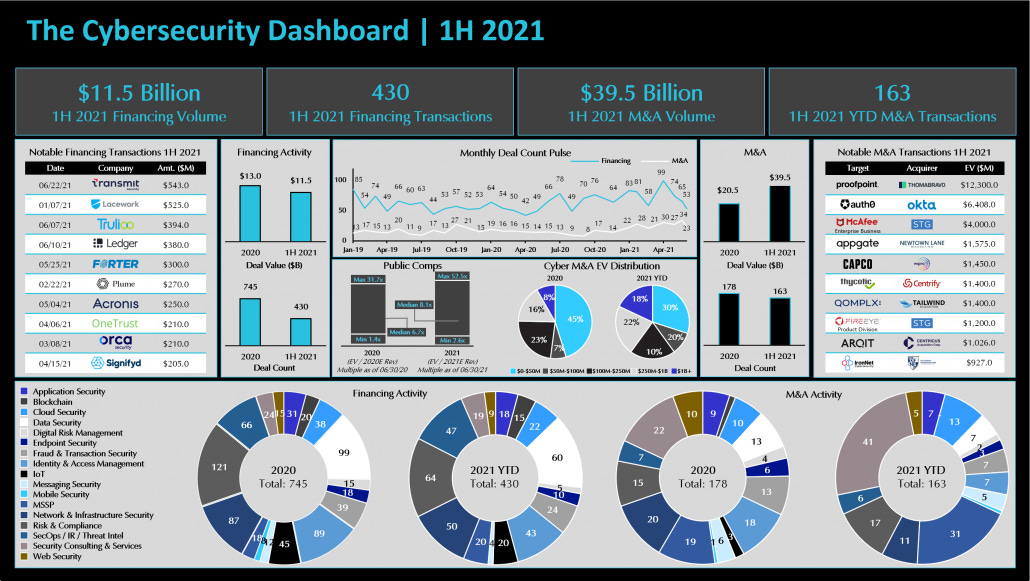

Huge Q2 in cybersecurity - check out Momentum Cyber report - a must read

The most active sectors for financings in the first half of 2021 included: Risk & Compliance (64), Data Security (60), Network & Infrastructure Security (50), & Security Ops & Incident Response (47)

What is developer experience?

Love it when The Economist covers enterprise infrastructure companies - great read on Databricks

The software-maker is soon likely to be known farther afield. Later this year it is expected to stage the largest-ever initial public offering (ipo) of a software firm—larger than that in late 2020 of Snowflake, its most serious rival. Alternatively, some predict, it could be snapped up by Microsoft in the largest ever software takeover. Whatever the outcome, there is substance to the hype. Databricks could become, in the age of artificial intelligence (ai), what Oracle and its databases once were in the world of conventional corporate software: the dominant platform on top of which applications are built and run.

I must say Ali is doing such a great job telling the story of why this is different and better than Snowflake without having to mention its main competitor

Yet Databricks only really took off when it added another component called “lakehouse”. It is a combination of two sorts of databases, a “data warehouse” and a “data lake” (hence the portmanteau). Both have historically been separate because of technical constraints and because they serve different purposes. Data warehouses are filled with well-defined corporate data that allow a firm to look into its past, for instance at how its sales have evolved, something called “business intelligence” (bi). Data lakes are essentially a dumping ground for all sorts of data that can reveal a firm’s future, including whether sales are likely to go up or down. Yet this separation is increasingly inefficient and unnecessary, explains Max Schireson of Battery Ventures, an investor in Databricks. “Doing bi and ai in different systems today is kind of stupid,” he notes.

🤣 some 💎 in 🧵

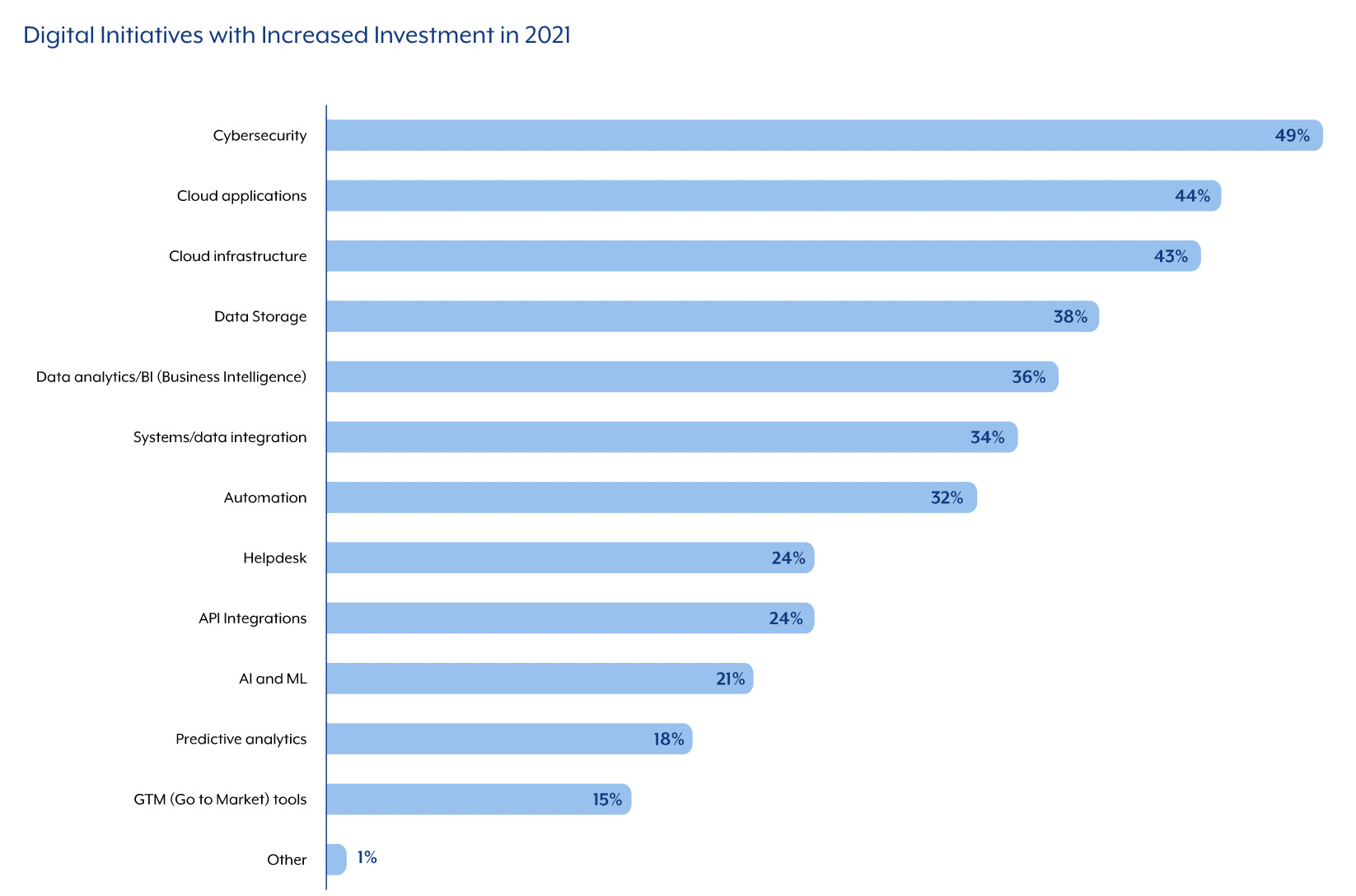

Workato State of Business Technology Survey is out and no surprise where the most 💰 continues to go in 2021

Blue Prism for sale in the automation space (FT)?

Blue Prism surged in value from less than £50m at flotation in 2016 to almost £2bn by mid-2018 over hype around robotic process automation, which transfers repetitive workplace tasks from humans to computers. And, as is normal when a fledgling business reaches a stratospheric valuation, professional short sellers gathered to pick at its numbers. Talk of cash burn and drifting targets for break-even soon eclipsed the sellside analysts’ total addressable market estimates, with the cynics zooming in on some unorthodox accounting around sales costs and a research and development budget that looked miserly relative to peers. By mid-2019, the stock had lost about two-thirds of its value.

Markets

Amplitude files S-1 and preps for direct listing

Founded in 2012, Amplitude provides product intelligence tools designed to help teams run and grow digital businesses. Amplitude records how users interact with a service via the web and native apps to create a detailed picture of activity.

Amplitude’s service brings together information collected from different platforms into a centralized dashboard that automatically organizes everything without the need for manual cleansing. Visual controls enable users to weave the individual data points into meaningful patterns.

Clients include a range of Fortune 100 companies, with notable customers including NBCUniversal Media LLC, Burger King, PayPal Holdings Inc., Peloton Interactive Inc., Cisco Systems Inc., Atlassian plc and Instacart.

For the year ended Dec. 31, Amplitude reported revenue of $102.5 million and a net loss of $23.7 million, or 98 cents per share. For the six months ended July 30, revenue came in at $72 million, up from $46 million in the first half of 2020, with a loss of $16.5 million, or 57 cents per share.

Okta (thanks Jamin!!!)

What’s next for Zoom?

Slamming the brakes on growth

In its Q2 earnings release, Zoom said for the current quarter it expects revenue of between $1.015 billion and $1.020 billion and earnings per share of between $1.07 and $1.08. Analysts polled by Refinitiv had predicted $1.013 billion in revenue and earnings per share of $1.09.

Perhaps more problematic for the company, though, is its significant slowdown in year-over-year revenue growth. In Q2 2020, Zoom saw its year-over-year revenue explode 355%. But in Q2 2021, revenue growth slowed to 54% year-over-year.

The slowdown was even starker when compared to the 191% growth Zoom saw in Q1 2021.

It’s not just revenue growth, though. User growth exploded for Zoom throughout the pandemic, with the number of customers with 10 or more employees skyrocketing 458% from 66,300 in Q2 2019 to 370,200 during the company’s Q2 2020.

That stratospheric increase, though, was never going to last. In its latest quarter, Zoom reported a 36% increase in customers with 10 or more employees, topping out at 504,900 such subscribers.